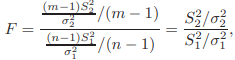

In Exercise 4.2.27, in finding a confidence interval for the ratio of the variances of two normal distributions, we used a statistic ![]() which has an Fdistribution when those two variances are equal. If we denote that statistic by F,

which has an Fdistribution when those two variances are equal. If we denote that statistic by F, ![]()

Exercise 4.2.27

Let ![]() be two independent random samples from the respective normal distributions

be two independent random samples from the respective normal distributions ![]() where the four parameters are unknown. To construct a confidence interval for the ratio,

where the four parameters are unknown. To construct a confidence interval for the ratio, ![]() the variances, form the quotient of the two independent χ2 variables, each divided by its degrees of freedom, namely,

the variances, form the quotient of the two independent χ2 variables, each divided by its degrees of freedom, namely,

(c) Rewrite the second probability statement as

We caution the reader on the use of this confidence interval. This interval does depend on the normality of the distributions. If the distributions of X and Y are not normal then the true confidence coefficient may be far from the nominal confidence coefficient; see, for example, page 142 of Hettmansperger and McKean (2011) for discussion.